Get ahead of the pack, make a smart budget

To kick-start your wealth journey, you need to have savings. Developing a proper budget will propel you on this journey. Let’s take a look at how you can implement a budget that is right for you.

What are the most common budgeting strategies?

To achieve your goal of implementing a smart budget, you’ll need to identify the best budget strategy for you.

There are three common budget strategies (others are typically a derivative of the three major strategies), 50/30/20 strategy, envelope strategy and zero-based strategy.

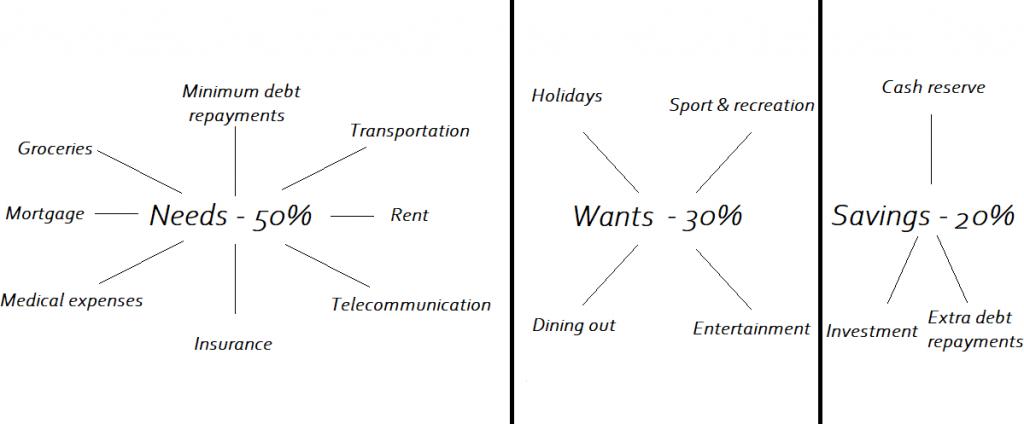

50/30/20 strategy

This simple-to-manage strategy is based on the premise that 50% of income should be spent on essentials (needs), 30% should be spent on discretionary items (wants) and 20% should be spent on savings.

While this strategy is less hands-on than envelope and zero-based strategies, it can still yield great results if it’s taken seriously. Plus, it’s great for people that have less time to manage their money and want to reduce budget complexities. This is because it reduces the number of sub-accounts you need to monitor and limits the need to manage every expense.

It simplifies the budget process and can be helpful to people that are unfamiliar with budgeting. If the money is available in the account, you can spend it. If it isn’t, you need to wait until the account is replenished. The most difficult thing to manage is determining the difference between your needs and wants, so make some rules and stick to them.

The 50/30/20 strategy is simple. Separate your needs, wants and savings and allocate a sub-account for each spending category. Need more than 50% for your bare essentials? Do it. Make the budget your own.

An envelope strategy should be designed so that it’s easy to follow and suits your needs. Design an approach that meets your needs, give it a try and modify as your needs change. Budgets aren’t set and forget.

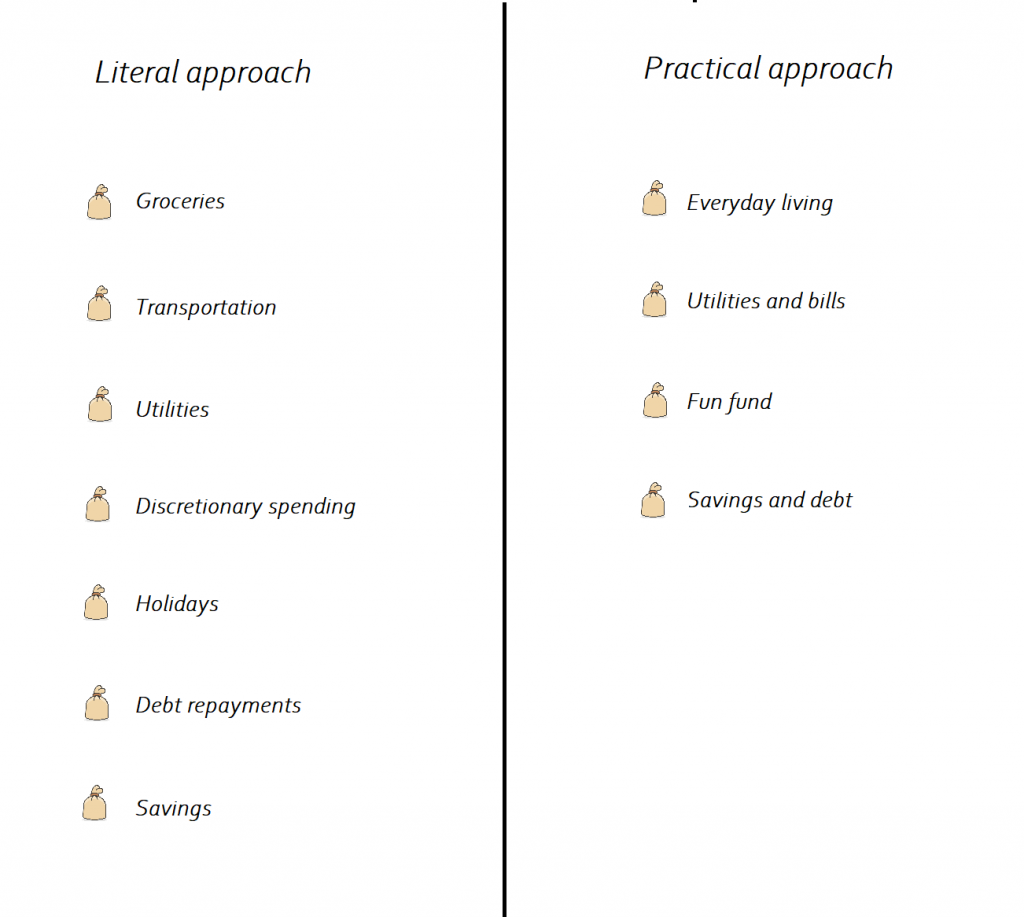

Envelope strategy

While an envelope strategy could literally be multiple wallets or envelopes each week (serving varying purposes), this strategy is now more commonly implemented with bank sub-accounts. Essentially, you assign categories to all your spending and determine the cost to maintain each spending category. You then transfer appropriate reserves to each envelope every pay cycle.

Should you run out of money from one envelope, you either stop making that type of purchase or shuffle money from a discretionary spending envelope. If you find this is occurring commonly, you may benefit from making the top-up permanent.

This strategy may take several months to properly implement. However, it’s less hands-on than a zero-based strategy and will still provide a very clear insight into your spending habits.

Similar to your choice of budget strategy, the way you manage an envelope strategy has to work for you, so tailor it to your personal needs.

Carefully consider practical ways to implement your strategy. Restrict debit card access to certain envelopes, like utilities, as this will reduce the chance of impulse purchasing occurring in the wrong envelope.

Envelope strategy

While an envelope strategy could literally be multiple wallets or envelopes each week (serving varying purposes), this strategy is now more commonly implemented with bank sub-accounts. Essentially, you assign categories to all your spending and determine the cost to maintain each spending category. You then transfer appropriate reserves to each envelope every pay cycle.

Should you run out of money from one envelope, you either stop making that type of purchase or shuffle money from a discretionary spending envelope. If you find this is occurring commonly, you may benefit from making the top-up permanent.

This strategy may take several months to properly implement. However, it’s less hands-on than a zero-based strategy and will still provide a very clear insight into your spending habits.

Similar to your choice of budget strategy, the way you manage an envelope strategy has to work for you, so tailor it to your personal needs.

Carefully consider practical ways to implement your strategy. Restrict debit card access to certain envelopes, like utilities, as this will reduce the chance of impulse purchasing occurring in the wrong envelope.

An envelope strategy should be designed so that it’s easy to follow and suits your needs. Design an approach that meets your needs, give it a try and modify as your needs change. Budgets aren’t set and forget.

Zero-based strategy

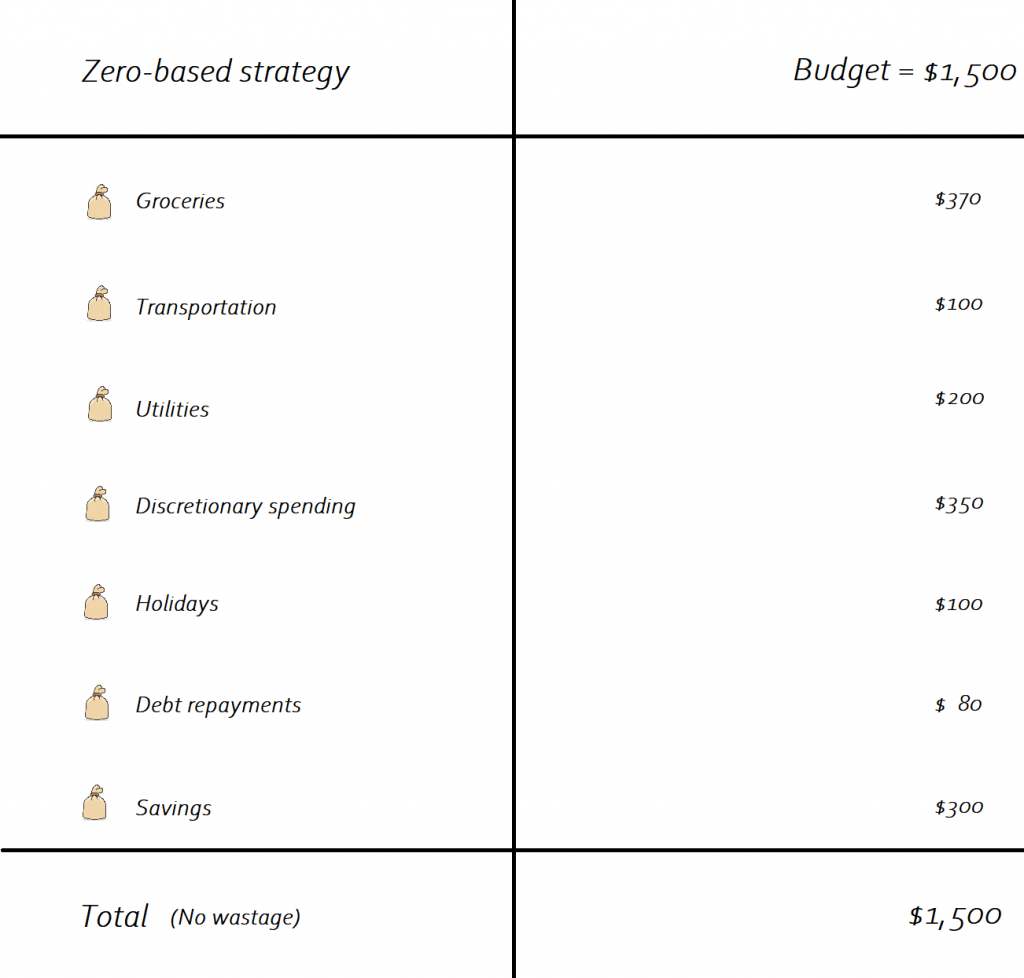

Popularised by YNAB, this is essentially an envelope strategy with a twist and is not for the faint hearted. It’s based on the principle that every single dollar you earn should be put to good use. So you delve deeply into your cost of living, envelope your expenses and identify how you will spend and save every single dollar that you earn, thus ensuring there is zero waste.

While the end goal (of having zero waste) is very rigid, the way you get there can be quite flexible. You typically start with necessary spending or savings and finish with discretionary spending.

You may also alter your savings and discretionary expenses at any particular time, allowing you to save or spend money on important discretionary expenses, like holidays, as needed. In this way, it’s a genuinely goals-based budget method – you set savings or spending goals and ensure that you hit them in the most efficient way

It takes time to manage your expenses in this manner, but those using this budget strategy have an unparalleled understanding of their expenses and a very good chance of achieving their goals.

A zero-based strategy doesn’t imply that you spend all your money. It is a strategy that allocates money to various specific allocations so that there is no expense wastage. The above example captures common categories, which would have further sub-categories.

How can I implement a smart budget?

Most importantly, budgeting shouldn’t make you miss out on everything you want to do. If you cut too many of the things you love from your spending, your budget is doomed to fail. Budgeting should focus on helping you to achieve what really matters to you, cutting expenses that you really don’t need.

With this in mind, focus on learning more about budgeting with free providers like moneysmart, which offer a range of tools, calculators and information. Using free resources is always a great way to start your budget journey.

Once you’re on your way, consider a range of reputable web-app providers (both free and paid services) that can assist you further. If you love the idea sub-accounts, seek a bank that provides them at no extra cost. And remember, budgeting is always popular for innovation, so there are plenty of options available to you.

For some, budgeting is a spreadsheet. For others, it is an app or sub-accounts. Regardless of the way you choose to budget, ultimately it’s up to you to manage your money in the best possible way and achieve the goals you set for yourself. In this way, the best budget strategy you can implement is the one that you will follow, so choose the one that is right for you.

About the author: Brenton has more than ten years experience in the financial planning industry. His specific qualifications include financial planning, margin lending, SMSF (self managed super funds) and direct shares. He is also an experienced investor.

Last reviewed: 7 July 2022

Do you want to keep up to date with the latest finance insights? It’s easy, subscribe today.

For more information about Investor Forecasts or any content on this page, please reach out to us.

The content and calculations of Investor Forecasts are for informational purposes only and are not provided as financial advice. They are not a substitution for professional financial advice and are to be used or relied on at your own risk.

You should make your own enquiries regarding any potential investments or other financial transaction you consider entering into. We strongly suggest you seek independent financial advice from a qualified adviser before acting or not acting on any information contained on Investor Forecasts.

We do not recommend disregarding the advice of such professionals because of something you have read, viewed, heard or calculations performed on Investor Forecasts.

Please refer to our terms of use for further information.