The truth about income and capital growth

Do you know the differences between income and capital growth? We investigate both types of investment return and why it’s important to build a portfolio of complimentary assets.

Capital growth

- Capital growth occurs when the price of a property changes.

- In Australia, it has the potential to be more tax-effective than income.

- You may use your capital growth to refinance loans and purchase additional investments, but you will need additional income to service any extra lending.

Income

- Income is received via rental payments.

- You may reinvest surplus income into other assets, improving portfolio diversification outcomes.

- As your investment income increases, your ability to service additional debt grows.

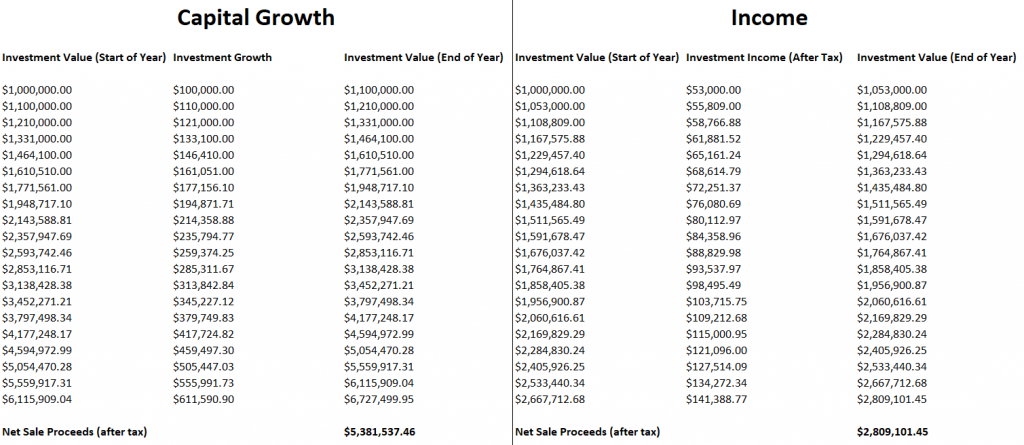

This example displays a 20 year forecast with a 10% p.a. return, 47% marginal tax rate, 50% capital growth discount and income reinvestment. As this marginal tax rate is high, the difference between the net after-tax return for capital growth and income strategies is very pronounced.

The impact of tax

In Australia, capital growth is often taxed concessionally. Individuals and trusts may qualify for discounting of up to 50% and super funds may qualify for discounting of up to 1/3 (both subject to conditions).

Investment income does not qualify for the same concessional treatment. Thus, an income investor may pay more tax and pay this tax at regular intervals.

This is the second significant difference. Growth investors do not pay tax on their growth until the asset is sold, whereas an income investor has paid tax regularly. This reduces their available income for reinvestment which reduces their asset-base and the subsequent financial return when compared to a growth-biased holding.

Therefore, the two ways that tax impact growth and income returns in Australia are:

- Capital growth may be concessionally taxed, whereas investment income does not qualify for the same concessions; and

- Investment income is taxed regularly whereas capital gains are allowed to accumulate without taxation until the asset is sold. This magnifies the achievable financial return for growth investors over time.

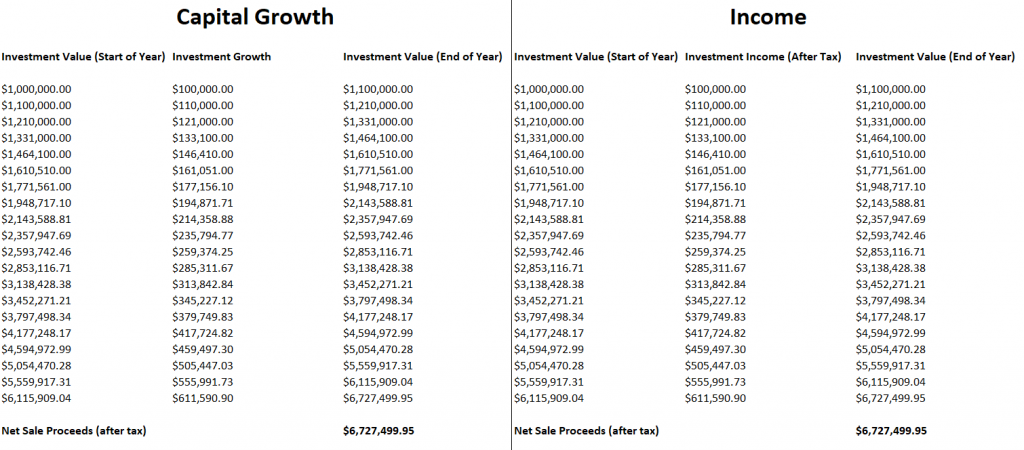

This example displays a 20 year forecast with a 10% p.a. return, 0% tax rate (such as in an account-based pension) and income reinvestment. As income is assumed to be reinvested and no tax is payable, there would be no difference in the after-tax investment return achieved. This highlights the only difference between these types of investment return, being how tax impacts the overall outcome.

Why invest for income?

The Australian property market is dominated by capital growth, rather than income. It is often easier to find properties that can grow when compared to properties that produce after-tax income. If this is the case, why invest for income at all?

Ultimately, income is important. If your portfolio doesn’t generate enough income, you may not be able to purchase more assets. This is because we rely on cash flow to meet portfolio costs, service debt and purchase more assets. You also need some protection against interest rate rises.

This is why income-producing assets compliment growth-biased investments well, as:

- Growth-biased investments are often negatively geared, reducing the income tax payable on your income-producing investments; and

- Income-producing assets assist you to cover your portfolio costs and allow you to access the equity that your growth-biased assets generate.

Essentially, using both income and growth assets will reduce the headwinds that you would otherwise experience if you only singularly target one type of investment. It’s therefore critically important that you consider balance within your portfolio before making each purchase. By doing so, you’ll not only accumulate great investments but also build a complimentary portfolio of assets.

SMSF – unique exceptions

While the above principles remain true for Self-Managed Super Funds, there are some additional factors that can make income or capital growth more attractive, subject to the strategy being undertaken.

Based on current legislation, you cannot access equity generated in a property within an SMSF to help purchase other assets. Therefore, SMSFs are entirely reliant on surplus cash flow or the sale of investments to fund further purchases. As such, this may make income producing investments more attractive where additional asset purchases are important.

However, there are also benefits offered for growth-biased investments within an SMSF. Based on current legislation, a property may be in-specie transferred into a CGT-free account-based pension when a condition of release is met. Therefore, an asset could be sold in pension phase without incurring any capital gains tax whereas it would otherwise have incurred tax at a rate of up to 15% if sold in accumulation phase.

These unique features make purchasing the right asset in an SMSF more complicated than one outside the superannuation environment. When combined with the many more complications associated with an SMSF, it is often necessary to seek professional advice prior to utilising this structure.

About the author: Brenton has more than ten years experience in the financial planning industry. His specific qualifications include financial planning, margin lending, SMSF (self managed super funds) and direct shares. He is also an experienced investor.

Last reviewed: 26 October 2022

Do you want to keep up to date with the latest finance insights? It’s easy, subscribe today.

For more information about Investor Forecasts or any content on this page, please reach out to us.

The content and calculations of Investor Forecasts are for informational purposes only and are not provided as financial advice. They are not a substitution for professional financial advice and are to be used or relied on at your own risk.

You should make your own enquiries regarding any potential investments or other financial transaction you consider entering into. We strongly suggest you seek independent financial advice from a qualified adviser before acting or not acting on any information contained on Investor Forecasts.

We do not recommend disregarding the advice of such professionals because of something you have read, viewed, heard or calculations performed on Investor Forecasts.

Please refer to our terms of use for further information.