How to best manage mortgage stress

With mortgage rates on the rise and cost pressures increasing on budgets across the country, it’s important pay serious attention to your mortgage. Let’s consider exactly what you need to do to navigate troubling financial times.

How can I avoid mortgage stress?

Borrow within your means

In Australia, mortgage stress is commonly considered to be where more than 30% of pre-tax household income is spent on loan repayments. The most significant thing you can do to avoid mortgage stress is to buy within your means. Borrow an amount that you can comfortably service.

Know your limits

We advocate for identifying your tipping point before you take out a loan. That is, identify the maximum interest rate that you can service before you are unable to meet your living costs. This will help you to understand your financial limitations and reduce ongoing stress as interest rates increase.

Have space in your budget to absorb multiple interest rate rises

Just because you have the power to borrow up to a certain amount, doesn’t mean that you should. Keeping debt repayments well below 30% of pre-tax household income must be a priority before taking out debt. Remember, interest rates rise to cool inflation, so you’ll likely have both cost of living and loan repayment pressures as interest rates increase.

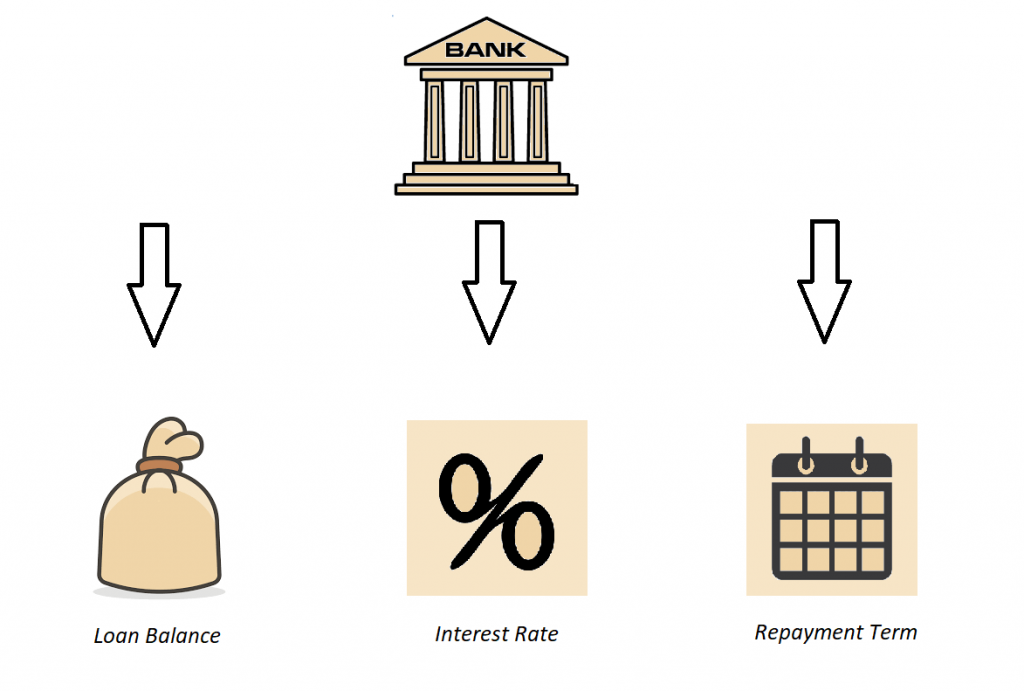

When calculating the repayment amount for a loan, a bank will consider the amount owed, the interest rate payable and the repayment term. Depending on the loan, additional loan fees may also be payable.

Get ahead, if you can

Whether it be with regular extra repayments to the loan or an offset account, getting ahead in good times can help if interest rates rise. This will provide a buffer that can be used to help when times are tough and you’ll also be more familiar with higher repayments, resulting in less hardship.

Repay your monthly repayments every four weeks

If you repay your mortgage monthly, consider transferring your repayment every four weeks. Why? You’ll make 13 “monthly” repayments, rather than 12. Not only will this reduce the interest payable, you’ll also repay your loan sooner too.

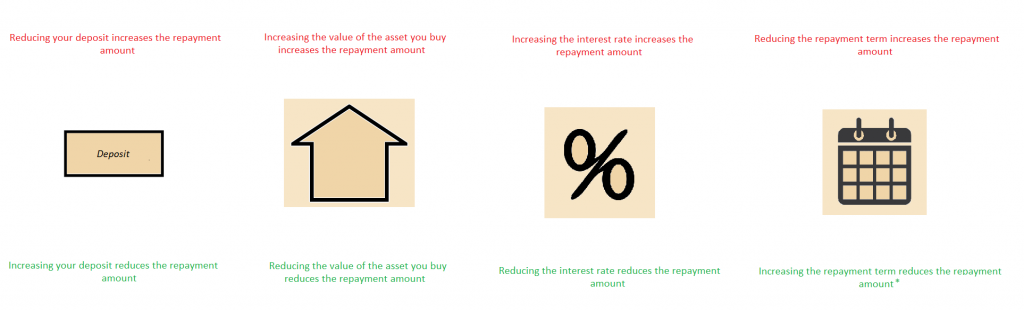

Changing components of your loan will alter the regular repayments that you will need to make. But remember, increasing the loan term will increase the length of time you hold a loan and potentially result in more interest being paid in the long term.

I’m stressed, and so are my finances! What can I do?

Shop around for a cheaper interest rate

Is your interest rate competitive in today’s market? It’s surprisingly common to be locked into high-cost loans, especially if you haven’t shopped around for some time. Loan markets are very competitive, so refinance to a loan that reduces your costs.

Reduce discretionary spending

Expenses are traditionally broken into four categories, necessary costs, discretionary costs, savings and debt repayments. Identifying your discretionary costs and reducing these expenses will provide additional capacity to meet your loan repayments.

Refinance your loan, potentially extending the repayment term

The loan term dictates the length of time that you repay the debt. Increasing the loan term reduces the regular repayment required for traditional principal and interest loans. While this can be a very powerful way to reduce repayments, this will result in you being in debt for longer and potentially charged more interest over the life of the loan.

Talk with your bank or a professional

Whether it be assistance with your budget or your loan, seeking professional advice may provide significant financial relief. With help, you may be able to reduce costs and navigate your way through tough times. Furthermore, having the right person on your side can provide real peace of mind, reducing stress during a difficult time.

Act before it’s too late

If times are tough, don’t let them get tougher. Take action while you have more options available to you.

About the author: Brenton has more than ten years experience in the financial planning industry. His specific qualifications include financial planning, margin lending, SMSF (self managed super funds) and direct shares. He is also an experienced investor.

Last reviewed: 21 June 2022

Do you want to keep up to date with the latest finance insights? It’s easy, subscribe today.

For more information about Investor Forecasts or any content on this page, please reach out to us.

The content and calculations of Investor Forecasts are for informational purposes only and are not provided as financial advice. They are not a substitution for professional financial advice and are to be used or relied on at your own risk.

You should make your own enquiries regarding any potential investments or other financial transaction you consider entering into. We strongly suggest you seek independent financial advice from a qualified adviser before acting or not acting on any information contained on Investor Forecasts.

We do not recommend disregarding the advice of such professionals because of something you have read, viewed, heard or calculations performed on Investor Forecasts.

Please refer to our terms of use for further information.